In most commercial real estate transactions, buyers understandably tend to focus on the economic terms – the purchase price, debt structure, and closing date. Those terms matter, but they are only part of the deal. Once a contract is signed, the due diligence period is the buyer’s opportunity to confirm whether the property can actually be used, financed, leased, operated, or developed for the purposes buyers intended.

In many deals, the most important issues are not obvious and do not come up during a site visit or by reading a rent roll. The important issues may appear in the title commitment, survey, leases, zoning records, service contracts, environmental reports, or closing requirements. Below are common diligence issues buyers should review before closing and why they are important.

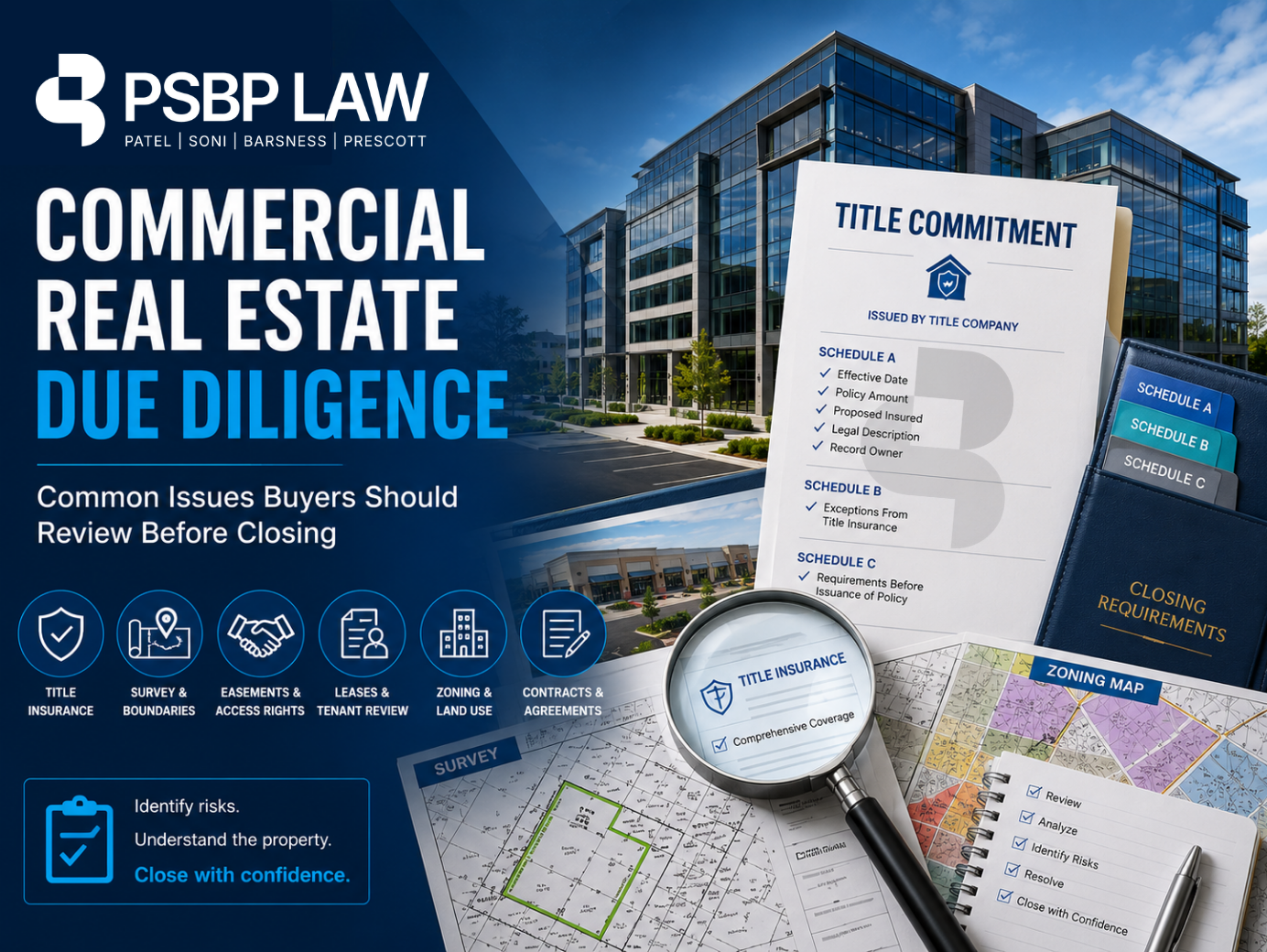

- Treating the Title Commitment as a Closing Formality

The title commitment is one of the most important pieces in a commercial real estate transaction. It identifies who is insured, the amount of money the policy insures, the legal description, the record owner, and the exceptions from title insurance that will affect the final title insurance policy.

Buyers should carefully review Schedule A of the title commitment to confirm the basics:

- The seller in the contract should match the record owner;

- The policy amount should be no less than the purchase price;

- The legal description should match the property the buyer intends to purchase (and be updated to match the survey).

A mismatch of any of these may be a simple drafting issue, but it can also indicate that the contract, survey, and title commitment are not describing the same property.

Schedule B is where many of the practical issues start to appear. This section lists exceptions to title insurance coverage, including recorded easements, restrictions, leases, utility rights, mineral reservations, rights of parties in possession, and other matters affecting the property. These exceptions should not be treated as standard boilerplate. Depending on the property and the buyer’s intended use, they can materially affect operations, access, parking, development, or financing.

- Not Reviewing the Survey Closely Enough

A survey can reveal issues that are not obvious from the title commitment alone. Common survey issues include encroachments, building lines, utility easements, boundary discrepancies, parking issues, and access concerns.

For example, an existing building may encroach into a setback line, a parking area may sit within a utility easement, or improvements may cross a property boundary. These issues do not always prevent a deal from closing, but the buyer should understand them before the objection deadline passes and it may be too late to address.

Buyers should also confirm whether the survey is current and representative of the currents state of the property, whether it is certified to the buyer, the title company, and any lender, and whether the title company will rely on it for purposes of the final title policy. In some transactions, an old survey may be acceptable with a survey affidavit from the seller. In others, a new or updated survey may be needed.

- Overlooking Easements, Restrictions, and Access Rights

Recorded easements and restrictive covenants can have a major effect on how a property is used. Some easements are routine utility easements, but others may limit where improvements can be built, require shared access, restrict parking, or give third parties rights over parts of the property.

Private restrictions can also matter. Older recorded covenants may include use restrictions, setback requirements, construction limits, or other provisions that no longer match how the property is currently being used. Even if a restriction seems outdated, it should still be reviewed during the title objection period.

Access should also be confirmed. A property may look like it has access from a public road, but the legal right of access may depend on recorded easements, shared driveways, reciprocal easement agreements, or rights over neighboring property. This is especially important if the buyer plans to redevelop the property, change the use, or rely on existing parking and drive aisles.

- Relying Only on the Rent Roll Instead of the Lease Documents

A standard Texas title insurance policy includes an exception for “rights of parties in possession”. This means that if a tenant in possession has a purchase option or right of first refusal that is not disclosed to the title company, the buyer may not receive coverage over such exception.

For income-producing properties, the rent roll is helpful, but it does not replace the lease documents. Buyers should review the actual leases, amendments, assignments, renewals, guaranties, and any side agreements.

Leases may include renewal rights, termination rights, purchase options, exclusive use rights, rent concessions, security deposit obligations, maintenance obligations, or restrictions on assignment. These terms can directly affect the value of the property and the buyer’s obligations after closing, and should be disclosed to the title company for the issuance of comprehensive coverage.

Buyers should also request tenant estoppel certificates when appropriate. Estoppels can help confirm the lease status, rent amount, security deposit, defaults, and whether the tenant is claiming any offsets or disputes. Without that confirmation, the buyer may be relying only on the seller’s records or representations.

- Missing Service Contracts and Operating Agreements

Commercial properties often have agreements that affect day-to-day operations. These may include maintenance contracts, laundry agreements, management contracts, utility agreements, equipment leases, trash contracts, parking agreements, or commission agreements.

A buyer should know which contracts will be assigned to buyer at closing, which will be terminated, and which require third-party consent. Some contracts may be minor, but others can affect revenue, expenses, access, tenant services, or future redevelopment plans.

If a recorded memorandum of lease or other agreement appears in the title commitment, the buyer should request the full agreement and any amendments. A memorandum usually provides only limited information, so it may not show the full term, renewal rights, termination rights, or other obligations.

- Waiting Too Long to Confirm Zoning and Intended Use

A property’s current use does not always mean the buyer’s intended use will be permitted. Buyers should confirm zoning, permitted uses, parking requirements, development standards, certificate of occupancy issues, and any local requirements that may apply.

This is especially important when the buyer intends to change the use, add improvements, redevelop the site, or lease the property to a different type of tenant. City ordinances, private restrictions, and recorded covenants can all affect whether the buyer’s plan is allowed.

If the intended use requires a permit, variance, rezoning, site plan approval, or other governmental approval, the buyer should identify that issue early in the diligence period.

- Not Tracking Schedule C and Closing Requirements

Schedule C of the title commitment lists requirements that must be satisfied before the title policy is issued. These often include payoff and release of existing liens, tax matters, entity authority documents, affidavits, deed requirements, survey affidavits, and other closing deliverables.

Buyers should review Schedule C carefully because unresolved requirements can delay closing or affect whether the seller can deliver title as required under the contract. Existing deeds of trust, judgment liens, tax liens, mechanic’s liens, or other monetary encumbrances typically need to be paid off or released at or before closing unless the buyer has specifically agreed to assume them.

It is also important to confirm who is responsible for each requirement under the contract. Some items are seller obligations, while others may require buyer cooperation, lender documents, or title company forms.

The Current Deal Environment

Commercial real estate deals continue to move quickly, and buyers are often under pressure to complete diligence, finalize financing, and close within tight timelines. That makes it important to calendar deadlines immediately and review title, survey, leases, contracts, zoning, and property-level diligence as early as possible.

The goal of due diligence is not just to find problems. It is to understand the property and make sure the buyer has a full and educated picture before closing. It also helps confirm that the buyer is getting what it expects under the contract. Identifying issues early gives the buyer the best chance to object, ask for a cure, renegotiate, obtain additional title coverage, or terminate before its rights expire.

If you are buying commercial real estate, we’re here to help guide you through the diligence process. Please feel free to reach out if you have any questions.